A Canary in the Coal Mine

Early Warning Signs of Distress in Private Credit Funds

A key advantage of private credit funds is their liquidity—or at least partial liquidity. Investors often have the flexibility to redeem their funds at will (as with publicly traded BDCs), at scheduled intervals (as with interval funds like CCLFX), or after a lock-up period.

This flexibility offers a significant edge over closed-end funds, which lack redemption options. However, it also places a greater responsibility on investors to actively monitor these investments. Why? Because you may want to exit those investments if warning signs emerge.

Today we will talk about five most common signs of trouble in private credit funds (with additional caveats that are specific to hard money lending funds). When you run across these signs, treat them as if the canary stopped singing: re-evaluate your position, and proceed with caution.

Where do you look for signs of trouble? In financial statements, of course. I urge you to ALWAYS review quarterly financial statement of private credit funds. “Pays like clockwork” doesn’t necessarily mean the fund is generating enough cash net interest income, if the fund is aggressively raising capital.

’s article is an excellent resource:

This article, along with the rest of our archive, is available exclusively to paid subscribers. Support our work: our newsletter is the only independent LP voice in a sea of sponsor-driven narratives!

Before we jump in, please note, the information provided is for informational purposes only and should not be considered investment, legal, or financial advice.

1. Delayed Audits or Financial Transparency Issues

Delays in reporting, lack of detail in financials, or opaque disclosure practices indicate potential mismanagement or trouble. This is generally not a problem with publicly traded BDCs or larger sponsors, but it’s a good practice to keep an eye on timeliness of reports, and transparency with all fund managers.

There is no excuse for not receiving a full set of financial statements: income statement alone does not provide meaningful information about cash flows of the fund. Review the cash flow statement, and pay special attention to interest income received as cash (as opposed to payment in kind, or accrual).

While we are on this subject, ALWAYS read auditor’s commentary!

2. Increasing Non-Performing Loans (NPLs)

A rise in NPLs or delinquent payments highlights operational stress in borrowers (or borrower companies):

Make it a habit to review loan tape: this lists all borrowers and the status of each loan.

Pay special attention to increases in NPLs (and read those auditor’s comments to find out at what point the fund manager recognizes them as such).

Some companies have tiers of NPLs (30-day, 60-day, etc; or Level A, B, etc) - monitor changes from quarter to quarter. If the late payers suddenly disappear, find out why. Borrowers could have re-negotiated loan terms, added past-due interest as payment in kind (PIK) and re-appeared on the performing loan list.

3. Increasing Payment in Kind (PIK)

Payment in Kind (PIK) refers to a type of financing arrangement where the borrower has the option to pay interest not in cash but in the form of additional debt or equity. Essentially, instead of paying periodic cash obligations, the borrower "pays" by increasing the amount they owe. Read this and this for more on PIK.

Non-performing loans (NPL) secured with real estate often have a similar feature. It’s less of an issue with such funds, which typically have much lower LTVs (and thus a wider margin of safety).

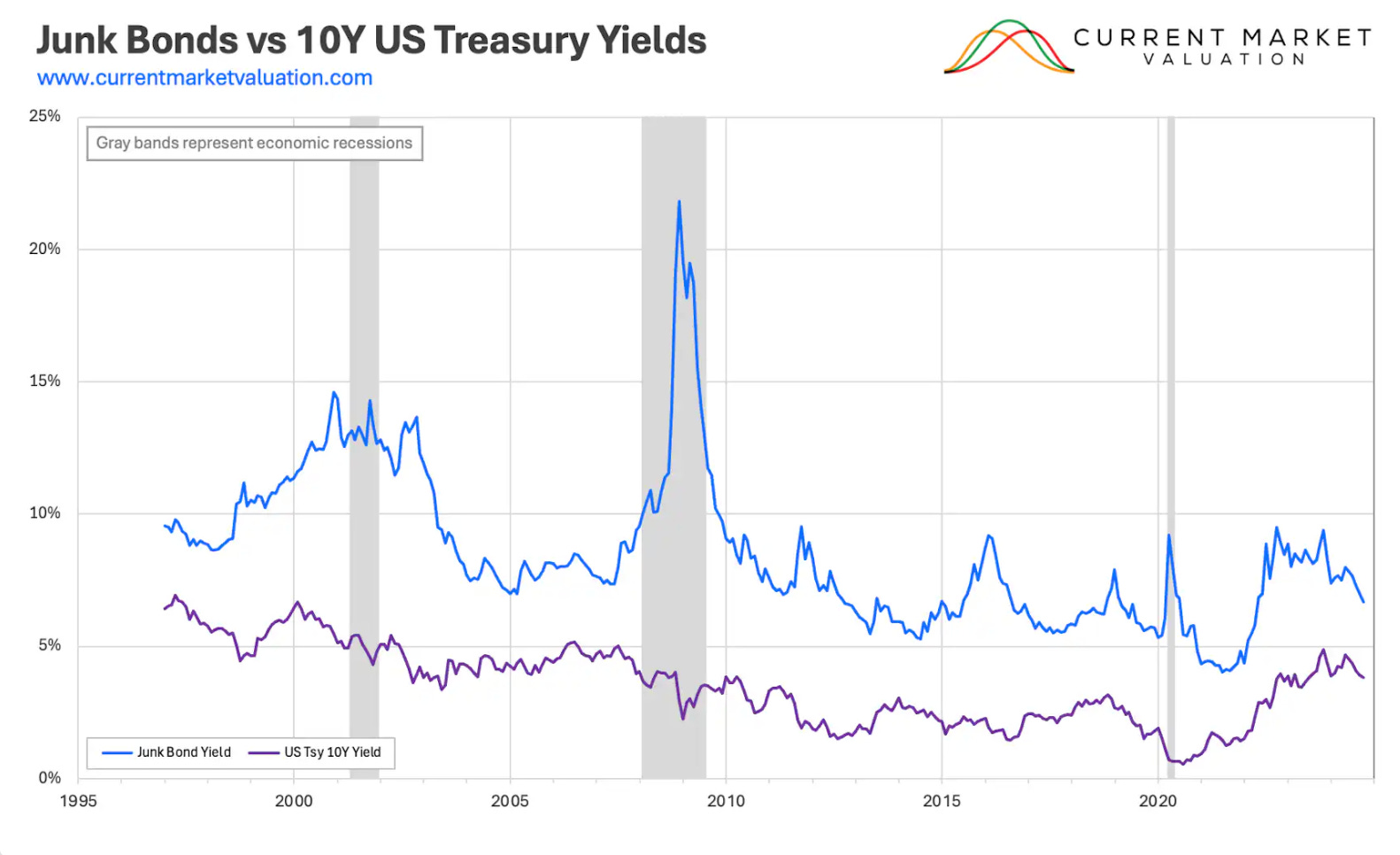

4. Widening Yield Spreads

Yield spreads move with the market: note how in the chart blow, high yield (aka junk bond) yields widened compared to the “risk-free” 10-year Treasury rates during recessions (shaded in grey).

That said, a fund offering higher-than-market rates may be taking on excessively risky loans to attract investors. Generally speaking, market for private credit loans is fairly efficient: higher risk borrowers will only be able to get loans at higher interest rates. Thus when a fund’s yield spread suddenly widens (while market rates remain the same), it’s prudent to ask whether this is due to deteriorating borrower quality.

5. Covenant Breaches or Waivers

Borrowers frequently breaching loan covenants or needing waivers signals declining borrower credit quality. This metric is difficult to track, because many such arrangements are not disclosed.

Remember our discussion on PIK? It can come in two forms: at loan origination, and as a “toggle” - when borrowers can elect to stop making regular interest payments and start accruing interest instead. Pay attention to the latter. A sudden increase in PIK interest could mean that many borrowers are electing this option (perhaps, due to being unable to meet debt obligations).

The next few points are specific to hard money lending funds. If you missed our article on how to perform due diligence, read it here:

6. Declining Loan-to-Value (LTV) Ratios on New Loans

Lower LTVs might indicate the fund is struggling to find quality borrowers or is taking on riskier loans. Most hard money funds are asset-based lenders, i.e. they don’t have very stringent borrower credit requirements. Investors’ margin of safety lies in the difference between the loan amount and the value of the property. You want this margin to be as wide as possible.

It’s a good idea to do a random screen of the loan tape: select a handful of loans, and review any publicly available information (Zillow, Redfin, etc) - check LTV, try to assess how much similar renovated homes sell for, etc.

7. High Default Rates and REOs

A noticeable increase in borrower defaults signals potential over-leveraging or poor underwriting standards.

For real estate owned, keep an eye on how long REOs sit “on the books” and how much profit the manager makes on sale. This takes a little work, but if you have financial records going back a few quarters, you can figure this out.

While private credit funds can offer attractive returns and liquidity, they demand active oversight to ensure your capital remains well-positioned. If there is one thing I want you take away, it’s this: review financial statements diligently, and pay attention to the canary song. Thank you for reading!

Another (no surprise) great article!

I spoke with an privated credit /BDC analyst who said that several years ago the SEC had a ruling that the BDCs could use present value and for defaults mark the value UP. I am not clear on it but from what I understand when it goes to default fees, and increase in interest rates are applied (like hard money) and the BDC can 'assume' that they will collect all of those fees in the future. The analyst said he has seen defaulted loans go up 7% in value. Have you or Kris any thoughts on this?