Multi-Family Preferred Equity [NO Deal]

Are You Asked to Throw Good Money After Bad?

*Some* preferred equity deals present a very attractive risk-reward scenario today, others are a ticking time bomb.

⚠️ Spoiler alert: today’s case study falls into the latter category.

The vast majority of preferred equity offerings today are effectively rescue capital into deals that may or may not be salvageable. Today’s No Deal (sorry for the spoiler) you’ll learn how to quickly screen these opportunities.

We will cover four key metrics to evaluate:

1️⃣ Purchase price & current value

2️⃣ Leverage & loan terms

3️⃣ Exit cap rate & repayment strategy

4️⃣ Free cash flow & source of distributions

The case study is inspired by several pitch decks I have received in the past few weeks. Don’t be surprised if you see more such offerings in the coming months: after reading this article you’ll understand why (that’s covered in point 5️⃣).

Accredited Insight is a unique newsletter: we are the only voice offering a perspective from the LP seat. We cover both the good and the not so good—such as questionable offerings—drawing on insights from hundreds of deals and numerous conversations with sponsors, LPs, and service providers.

By becoming a paid subscriber, you will gain access to our database of over 30 case studies and articles on everything you need to know to become a better investor. If you are a GP, this is your window into the world of capital allocators. Click the button below and chose your preferred term: you can pay $10/month or $100 for a full year.

Deal or No Deal?

Please remember, the deal is presented as a case study, and all relevant information has been changed to protect the identity of the sponsor. This is not investment advice.

Brief recap of the deal:

This is a preferred equity offering. If you don’t know what “preferred equity” means, and where it sits on the capital stack, read this first:

Effectively, this fund is raising equity to come in preferred position into existing deals. As a side note: some preferred equity funds provide capital at the time of acquisition—but that’s not the case for this one.

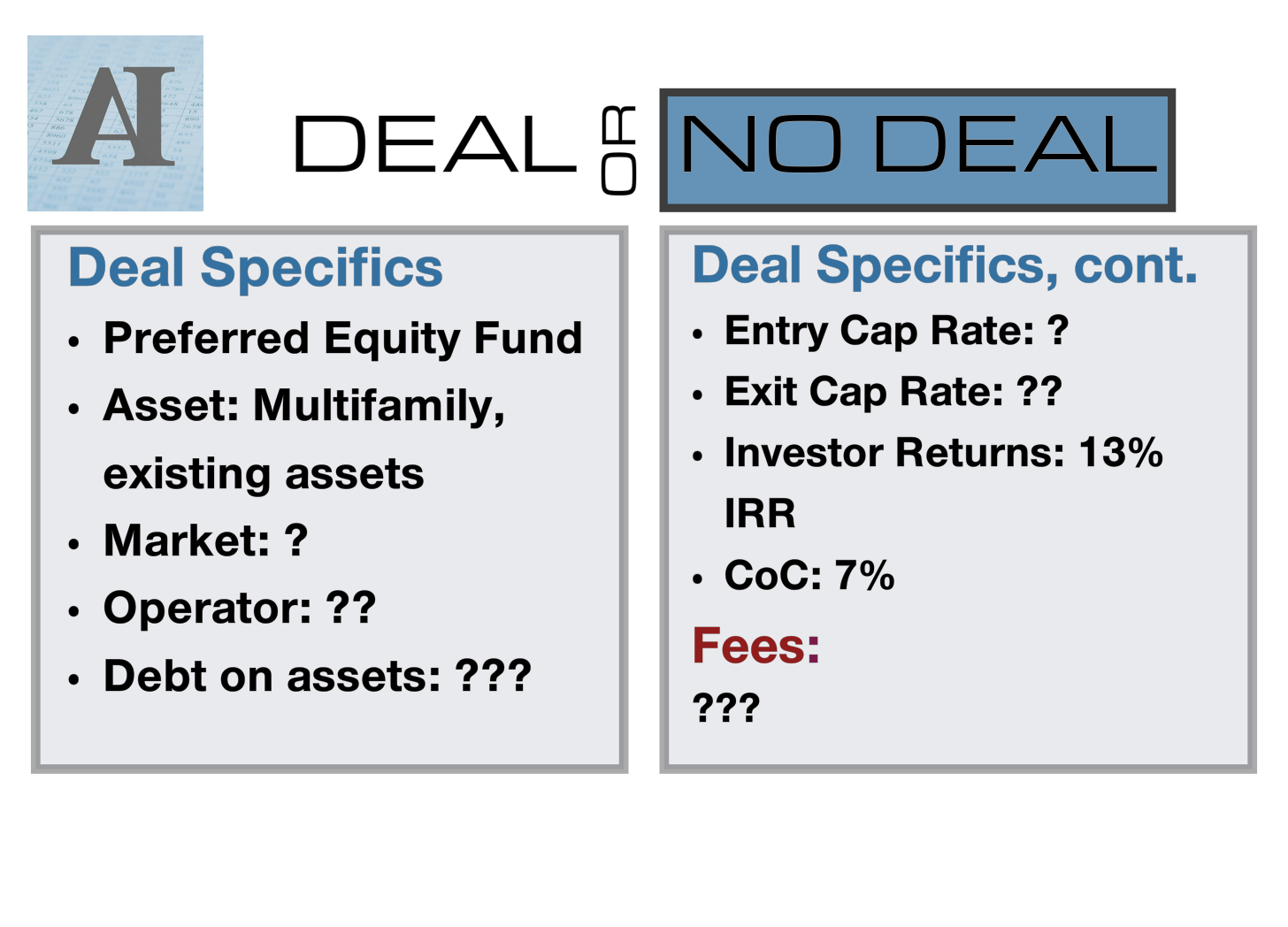

You see all the question marks in the visual above?

— That’s all the information missing from the deck.

Why do you need to know all of it, if the pref equity fund promises to pay you 7% current yield? Because you MUST understand the source of said distributions.

But I’m getting ahead of myself. Let’s walk through the steps of analyzing such deals.

1️⃣ Purchase Price

I’m going to throw a 💣 here.

If the properties in the fund were purchased any time after 2021, chances are they are currently worth less than purchase price. In many instances, they are worth less than the loan balance.

How do you estimate this? Start with property-level NOI, compare it to the NOI at acquisition, and apply a reasonable cap rate to get a valuation.

If the estimated value is significantly higher than the loan balance, you can proceed.

If not, you may be looking at a deal that’s already underwater.

2️⃣ Leverage (Debt on Assets in the Fund)

This bucket has many items - all of them important.

Loan details: balance, maturity, floating or fixed rate, rate caps (cost and expiration), is it being extended or refinanced, etc. Fuzzy on terms? Review this:

LTV: you’ll need to know loan to value ratio at acquisition, and an estimated present LTV (use your guesstimated value from step 1️⃣).

Debt Service Coverage Ratio (DSCR): annual cash flow before debt divided by total debt service. Calculate this with and without rate caps.

3️⃣ Exit Cap Rate

Figure out how preferred equity will be paid back. Yes, this sleeve of equity is higher on the capital stack, but:

‼️ higher on the capital stack ≠ safe investment

There are only two ways the payoff will occur:

Refinance

Sale of asset. (If the asset sells for the loan balance, being “preferred” doesn’t mean you’ll get your money back).

Your job is to figure out how likely those scenarios are - and in either case, you need to know the GP’s exit cap rate assumptions.

4️⃣ Free Cash Flow (Source of Distributions)

Repeat after me:

Receiving regular cash flows ≠ deal is performing well

The easiest way to ensure regular distributions is by over-capitalizing the deal. This means the property might not generate enough cash flow to meet a 7% yield, but the sponsor raises extra money and puts it in reserves to cover distributions for a year.

As an investor, you must know the true source of your distributions.

🧮 To check this, run the numbers using the P&L. It’s straightforward: calculate the excess cash flow (after debt service and sponsor fees), then compare it to the total preferred equity and yield. If there’s anything left over, divide that by the total common equity to determine the common equity yield.

5️⃣ Expect More Such Deals (or Why You Should Be Wary)

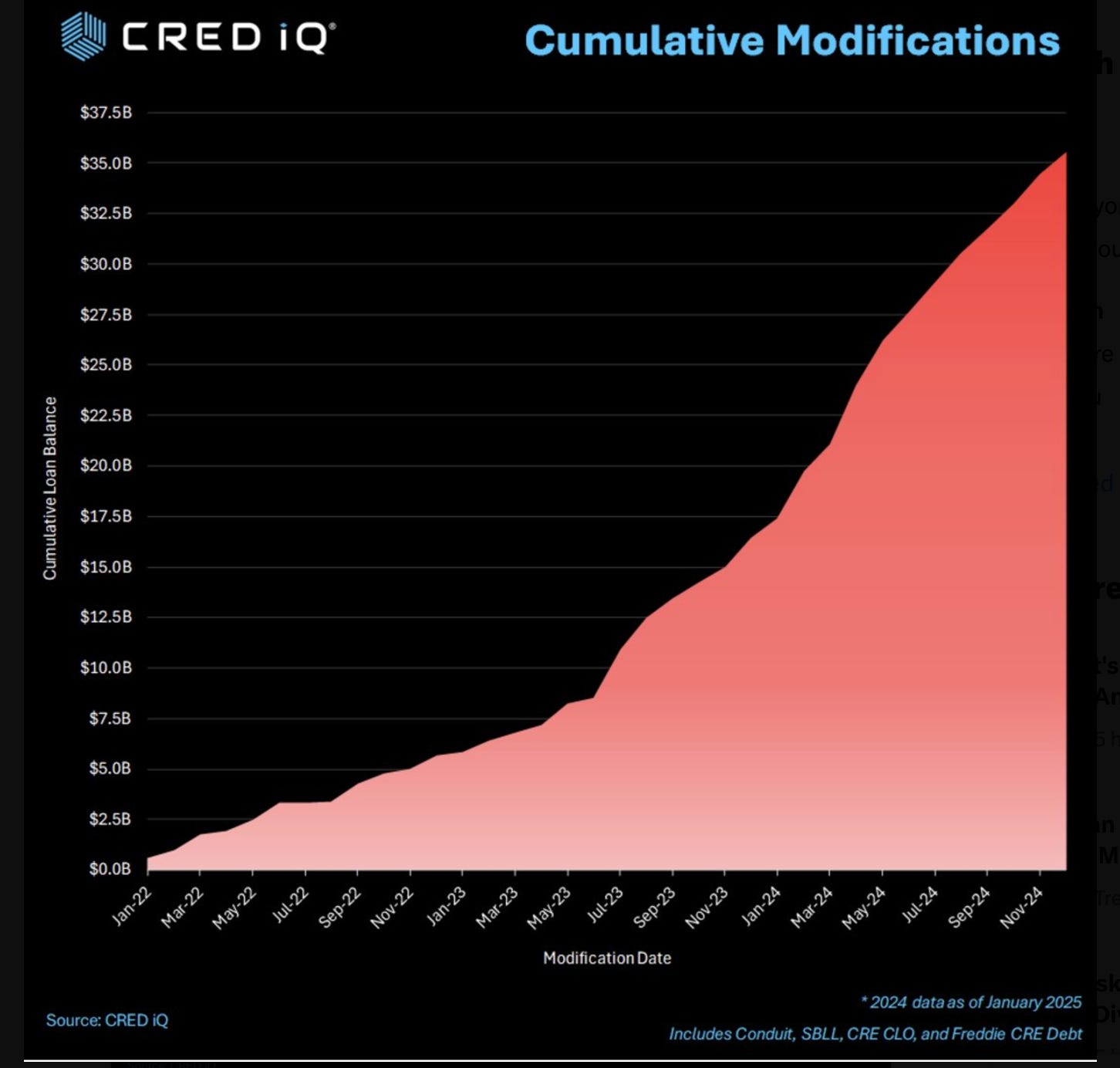

We’ve written extensively about the upcoming maturity wall, and the bridge loan fiasco (here). Here’s a very brief recap of what is currently happening:

Many deals financed with bridge loans between 4Q2021 - 2023 are underwater (property value < loan balance).

Many such loans have expiring rate caps

Many such loans have DSCR below 1.0x (without rate caps)

Lenders are reluctant to take possession of these properties - hence the flood of extensions and loan modifications:

Borrowers often don’t have the capital to purchase new rate caps, and are either unable or unwilling to call capital from existing equity.

Ergo, “preferred equity” offerings.

❓Have you come across preferred equity deals? What’s your take on the current market? Please leave a comment below!

Bottom Line

Not all preferred equity deals are created equal. Some offer solid risk-adjusted returns, while others are just disguised rescue capital. As always, ask the right questions, and don’t chase yield blindly.

We hope you learned something from this case study. Please share with your fellow investors if you found this helpful! The full database of our case studies can be found on the front page.

Scariest investments right now are broken operators sourcing $ for OpCo level funds that aren’t collateralized by any single asset.

Excellent writeup! Especially: higher on the capital stack ≠ safe investment I have spoken to people who are chasing PREF Equity "opportunities" thinking they are "safe". Leyla's writeup, applied properly, probably eliminates most of the deals us LPs are seeing. Also, I wonder if the institutional pref equity firms see the better quality deals vs. an LP such as myself who gets a deal forwarded to their mailbox?