Multifamily Preferred Equity Case Study

What an old banker can teach you about evaluating preferred equity deals

A looooong time ago, when borrowing money meant going to a bank, and I was bright-eyed and bushy-tailed, a mentor taught me the three Cs of credit: collateral, capacity, and character. As a banker, he evaluated each separately and famously said, “When you lend money, the only time you really need to worry is when the borrower lacks the last one.”

Why am I telling you this in an equity case study? Because preferred equity is like a mutant mezzanine loan: it has limited upside but no lien on the property. That means preferred equity deals should be evaluated based on the borrower’s ability to repay the obligation, and the collateral securing said obligation.

Today’s case study is another recapitalization (remember this case study? it was a recapitalization presented as a new purchase). The twist: proceeds will be used to pay off existing preferred equity. The structure of the capital stack remains the same—debt plus two classes of equity.

If you need a refresher on capital stacks, this will help:

Before we dive in:

Accredited Insight is a unique newsletter: we are the only voice offering a perspective from the LP seat. We cover what we see and what we learned in private markets, drawing on insights from hundreds of deals and numerous conversations with sponsors, LPs, and service providers.

By becoming a paid subscriber, you will gain access to our database of over 30 case studies and articles on everything you need to know to become a better investor. If you are a GP, this is your window into the world of capital allocators. Click the button below and chose your preferred term:

Deal or No Deal?

Just a friendly reminder: this is for educational purposes only, not financial advice. Numbers, location, and details have been changed to keep the sponsor’s identity confidential.

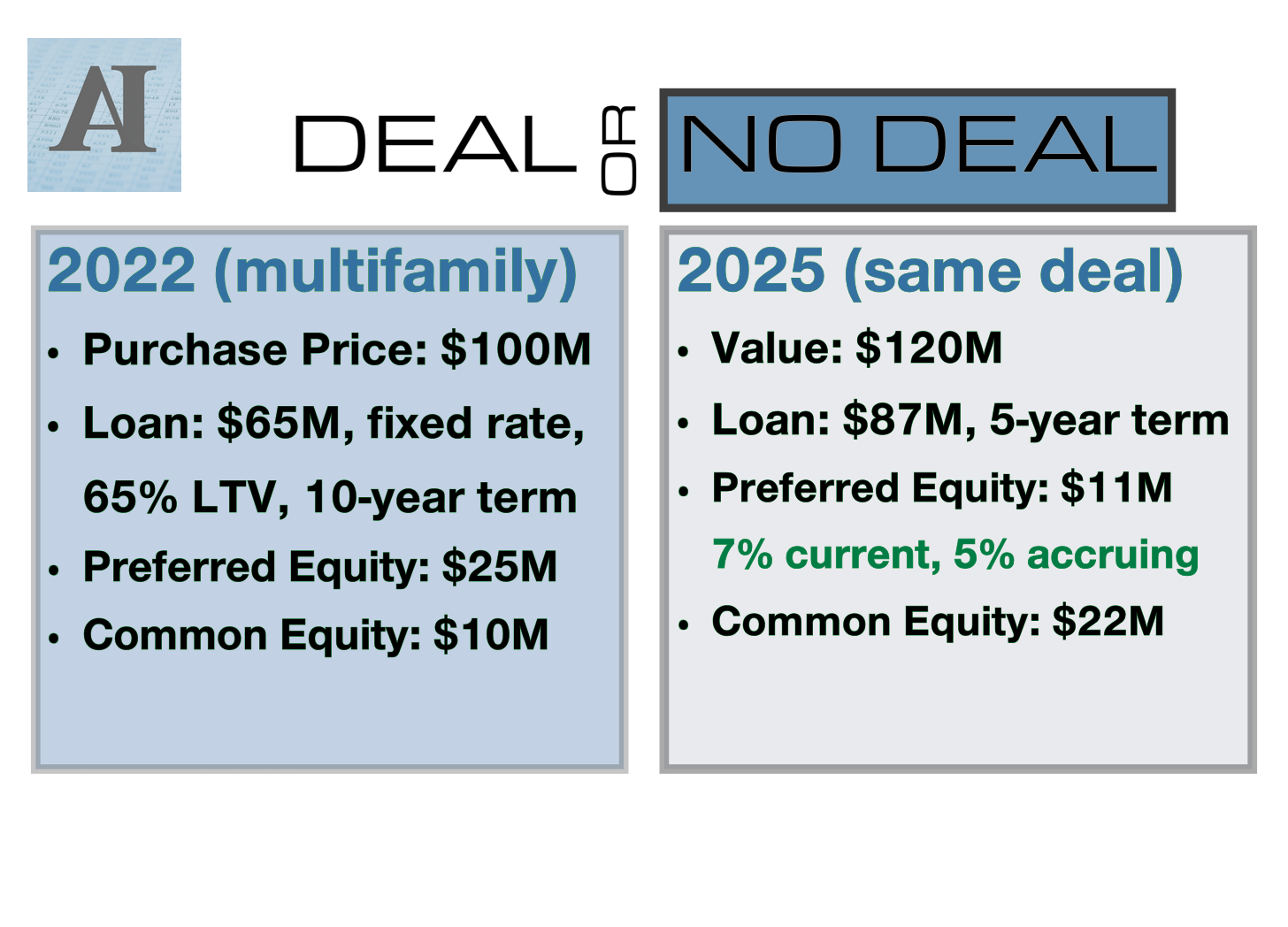

Deal Summary

The multifamily property was originally purchased in 2022 with a 10-year fixed-rate loan and two equity classes (preferred and common).

In 2025, the deal is being recapitalized. The loan is being refinanced (likely at a much higher interest rate), but there aren’t enough proceeds to pay off the 2022 preferred equity (in 2022: loan + preferred equity = $90M). So, the GP is bringing in new preferred equity instead.

Let’s analyze this using the banker’s framework: collateral and capacity (to repay). As for the third and most important C, character, you’ll have to assess that yourself.

Collateral 🏢

With any recapitalization, your first question should be: How was the asset valued?

Decks often state something vague like “The property was valued at $X by the lender.” That doesn’t tell us much. Lenders today are far more constrained by debt service coverage than LTV.

Since this deck provides no financials (we don’t know the NOI), we’ll go with the given numbers and use the $120M valuation. The senior loan has an LTV of 72%. Is that high? Yes. If you don’t know what high leverage can do to your equity, read this:

Now, let’s add new preferred equity to the loan amount. We get to CLTV of 82%. That means there isn’t a very wide margin of safety behind preferred equity.

Capacity 💰

The next question: can the borrower repay the loan?

In this case, the GP is offering a 7% quarterly yield plus 5% on exit. But let’s evaluate how durable that 7% is.

We don’t have a pro forma or trailing 12 month’s numbers (which is a shame). The only data provided is the debt service coverage ratio (DSCR) of 1.25X for the senior loan. There’s no DSCR info on the preferred equity sleeve, but we know one thing for sure: It’s less than 1.25X.

So, let me ask you: if the absolute minimum a bank will accept is 1.25x (and they have way more information than you do), why would you settle for less?

One final question, out of sheer curiosity, but possibly the key to this deal: Why is the GP bringing in equity instead of a mezzanine loan? Remember, the loan they got in 2022 has a fixed (likely low) rate and another 7 years remaining. They are paying it off instead of getting a supplemental loan.

Two possible reasons (lenders, drop your thoughts below, in case I’m missing something):

A mezz lender would charge more than 12% for this level of risk, so going the pref equity route is cheaper.

There aren’t many lenders willing to finance a deal where DSCR is toeing the 1.0X line.

I’ll leave you with this: preferred equity deals today are all over the place. There are some great ones out there, but they’re few and far between. Do your due diligence. Please don’t assume every “preferred” equity deal is “safe”.

Thank you for reading! Have a wonderful week - and subscribe, if you haven’t yet.

What were the terms on the original preferred equity? This deal would make me suspicious as F.

Assuming the rate only increased 300 basis points, we're looking at approximately 3% * 7 years equals 21% of the loan value. So in this transaction we would ballpark that the borrower is forfeiting the net present value similar to 21% of 65 million.

Given that 65 million is such a large portion of the financed amount losing 21% of it would be an enormous loss. That's 13.65 million on an original total property value of 100 million.

Given cap rates today and the cost of that new loan (just approximating), the new loan interest rate probably exceeds the cap rate. So the preferred equity coverage is awful. The common appears to be trying to withdraw all of their original investment, even at the cost of crippling future cash flows by sticking it with a high rate of debt.

If this was a real deal or the terms were very similar to a real deal on a proportional basis, then I would be inclined to think the manager was screwing the investors long term (by losing the value of the fixed rate loan) to churn that money faster or leverage it harder to bring in more management fees.

What do you think?

Also, this is probably the best real estate Substack. There are good ones for REITs, but your work on the underlying real estate is my favorite.

Wooof...this is a "hell no" for me. The general feeling at last week's Old Capital MF session is that "extend & pretend" is coming to an end and distressed operators have no place to turn, other than maybe suckering in investors chasing yield with financially engineered schemes such as your case study above.