Private Credit (Non-Traded BDC): A Valuation Black Box

How fund managers mark their loans—and what investors need to watch for.

It’s February 2025.

By now, every investment bank has declared this $3 trillion asset class to be in its golden era.

And at long last, Bloomberg has caught on:

To mark this momentous occasion 🎉, today’s Deal or No Deal case study is a private credit fund (feel free to forward this to the Bloomberg team).

We’ll touch on a few factors every investor in private credit should evaluate (and discuss what I really want to talk about at the end):

✅ Borrower Risk – how strong are the companies taking on debt, and what protections are in place for lenders?

✅ Manager Risk – does the fund’s management team have the experience and discipline to navigate credit cycles?

✅ Macro Risk – how do external factors like interest rates and economic conditions impact the fund’s performance?

✅ Fund Structure & Leverage – what kind of capital structure does the fund use, and how does that impact investor risk?

✅ Liquidity – can investors exit the fund when needed, or is capital locked up for extended periods?

Each of these categories is discussed in depth here:

Before we dive in:

Accredited Insight is a unique newsletter: we are the only voice offering a perspective from the LP seat. We cover what we see and what we learned in private markets—drawing on insights from hundreds of deals and numerous conversations with sponsors, LPs, and service providers.

By becoming a paid subscriber, you will gain access to our database of over 30 case studies and articles on everything you need to know to become a better investor. If you are a GP, this is your window into the world of capital allocators. Click the button below and chose your preferred term:

Deal or No Deal?

Please remember, this information is for educational purposes only and should not be considered as financial advice.

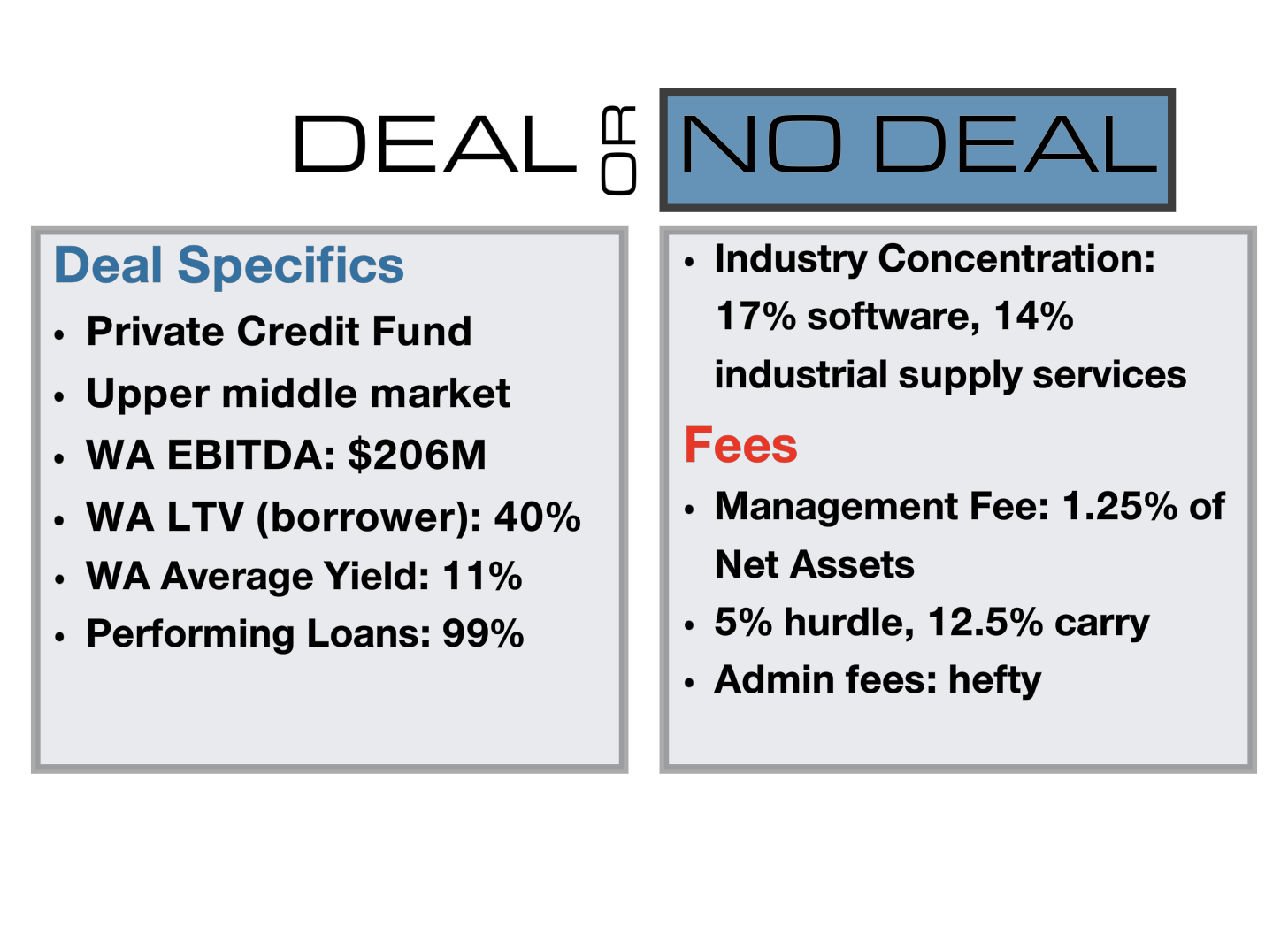

Today’s case study is a private credit fund that lends to upper middle market companies - weighted average EBITDA of borrowers is $206M . The fund is set up as a non-traded BDC (which means it has to distribute a certain percentage of income, but is not listed on a public exchange).

The real focus today? How this fund values its loans.

But first, let’s do a quick screen. (This is not full due diligence!)

📌 Borrower Risk:

Lending to upper middle-market companies generally carries lower risk than smaller borrowers.

High concentration of software companies—not ideal, as many could be unprofitable.

40% weighted average LTV—standard for this market.

96% first-lien debt—a positive.

99% of loans are current—also a good sign. But this begs the question as to how the fund determines “non-performance”

PIK income is rising, with 13% of dividend income accrued as PIK—worth watching.

📌 Manager Risk:

Firm founded in 2007, fund launched in 2022. Would want to see how the firm performed during and after the Great Financial Crisis.

As always—spend your time on doing due diligence on the fund manager!

📌 Fund Structure:

Non-traded BDC, so investors typically pay fees to access it (often via RIAs).

Leverage is ~1.75x (Total Assets/Net Assets).

No debt maturities in the next 24 months. Debt is a mix of floating-rate credit lines and fixed-rate notes.

Cash Net Investment Income Coverage = 95%—I prefer to see 100%+. There is a plethora of reasons why. Read the article below, if you’d like a deeper dive:

Valuation of Assets

What I really want to talk about today is how the fund values its assets—specifically, the loans it’s made to upper middle market borrowers. This is where things get murky. Last week, I wrote the article linked below. It inspired today’s case study.

This is a quote from the financial statements:

“Note 5. Fair Value Measurements

The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).”

What does this mean?

Level 1: Think stock prices on the NYSE—direct, unadjusted quotes from active markets.

Level 2: A step removed—uses observable data, like prices of similar assets or market-derived inputs.

Level 3: The wild west—no direct market data, just estimates and assumptions from the fund manager.

Where does our fund stand?

According to its SEC filings, 89% of its assets are classified as Level 3. That means the vast majority of these loans—first-lien or otherwise—don’t have a readily available market price. The manager has to rely on models, projections, and judgment calls to come up with a value on them.

‼️ Now, I’m not saying this is inherently bad—we are dealing with an illiquid asset class, this is par for the course. But this setup raises a question: How accurate are these estimates when there’s no active market to check them against?

This story is a cautionary tale about what happens when a private credit fund holds illiquid assets at valuations that have little semblance to reality.

What are your thoughts? Let us know in the comments.

Going to be interesting to follow the trends in valuation for these non-traded BDCs. The amounts being raised are staggering. I wrote about it in my piece last week on the democratization of private credit.

Wow, Leyla. Even honest persons of integrity cannot think straight when they have strong incentives toward some outcome. Our emotions are just too involved in the thinking process. I see no reason to believe evaluations by the fund or manager of those Level 3 assets.

Thanks for the look under the covers.