The LP’s Escape Hatch: Unlocking Liquidity with Secondary Funds

How Institutional Investors Navigate the Secondary Market—And What You Need to Know Before You Succumb to the Siren Call

Ever wish you could “undo” some LP investments?

Yeah, me too. There are some LP investments I’d love to offload. You can take a wild guess about my satisfaction with their performance, I’ll leave that to your imagination.

Unfortunately, I am not a pension fund: I don’t have a ready exit. Institutional investors, however, do.

Enter the secondary market—a space where LPs can sell off fund commitments, gain liquidity, and sometimes accelerate returns (or so the pitch decks claim). But as with many things in private markets, nuances abound and your results may vary.

In this article we’ll break down:

✅ The essentials of secondary funds

✅ How they work

✅ Their advantages and risks

✅ Key due diligence steps for investors

📚 You’ll find the list of white papers and reports at the end of the article.

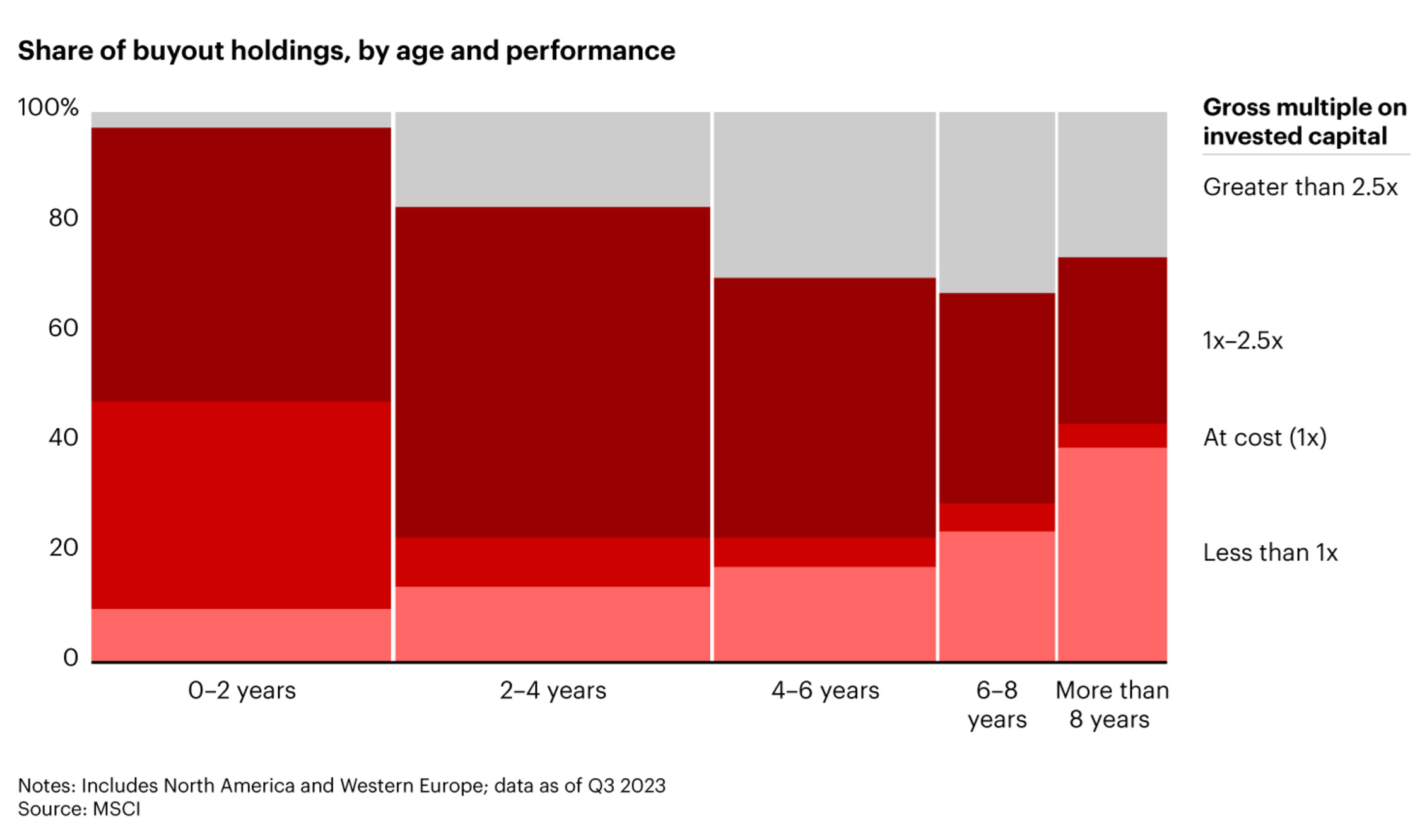

‼️ Before we get going, take a close look at this chart. Which LPs are most eager to exit their investments and redeploy cash? And which companies are GPs looking to sell so they can move on and raise the next fund?

🔎 What Are Secondary Funds?

“Secondary funds have been around since before the global financial crisis. They started as pools of capital formed to let LPs sell GP positions when they needed cash faster than GPs could provide it. In those early days, growth was limited by the stigma attached: Abandoning a GP was akin to acknowledging you’d somehow made a mistake.” - Bain & Company

Unlike primary private equity funds, which invest directly in companies, secondary funds acquire existing commitments in private equity vehicles. In essence, they provide a market for investors (LPs) seeking liquidity by purchasing their stakes, often at a discount (hold this thought for a minute - this is important!)