The Slow Erosion of Illiquidity Premium

Are you getting paid enough for not having access to your funds?

Imagine waking up tomorrow with a (legally obtained) $20 million burning a hole in your pocket. You want to invest before your spouse convinces you to buy that villa in Italy.

You have two choices:

Buy shares of a publicly traded company, or

Invest in a privately held business, locking up your money for at least ten years.

If these two investments have identical growth prospects, you'd expect higher returns from the private stake to compensate for its illiquidity, right? This is illiquidity premium, once a major draw for private market investors.

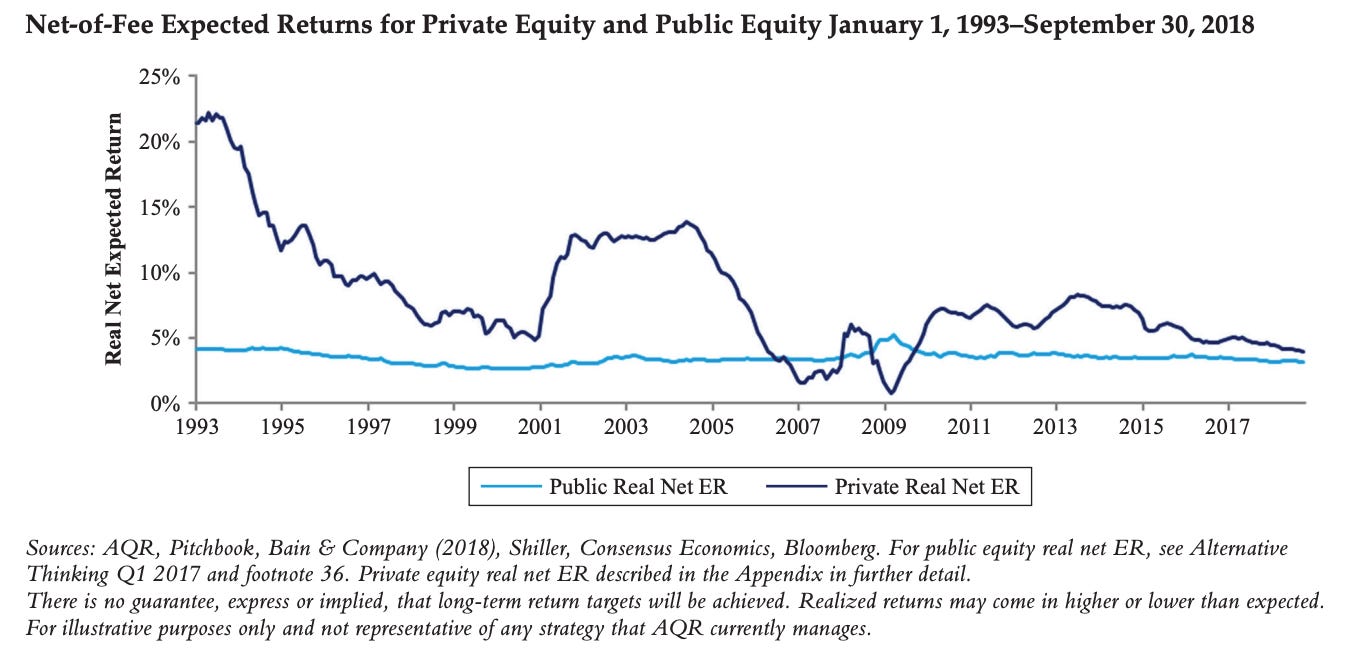

And historically, this premium has been meaningful. Take a look at private equity's expected returns in the '90s, when only institutional investors had access to private markets. It's no wonder everyone wanted a piece of the action.

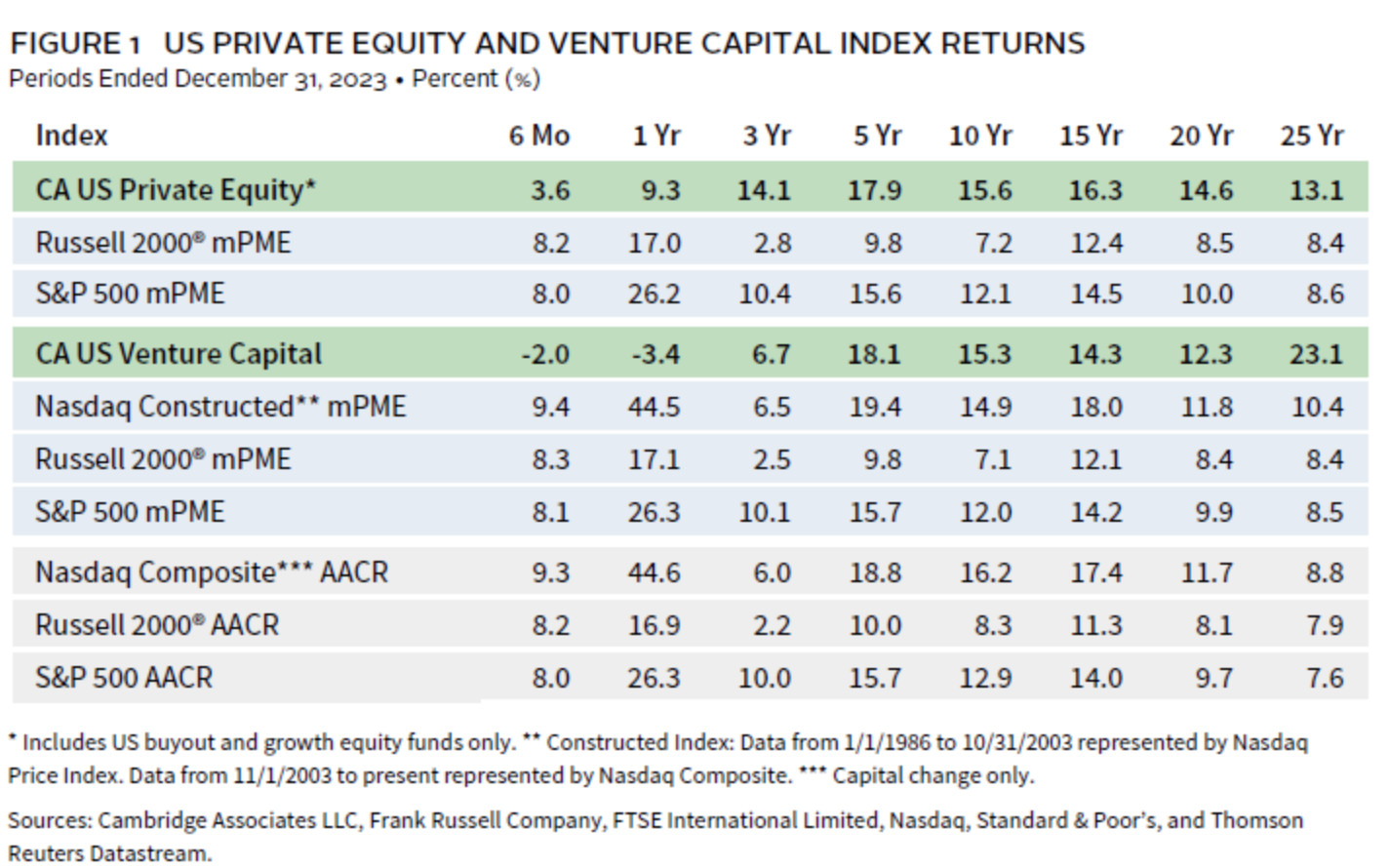

However, over time the returns have slowly converged. And over the past three years private equity and venture capital have actually underperformed their public market counterparts.

While the S&P 500 and NASDAQ have delivered exceptional returns fueled by a handful of mega-cap tech stocks, many private market funds have struggled with challenging exit environments, extended holding periods, and downward valuation pressures.

This underperformance raises serious questions about whether investors are being adequately compensated for surrendering liquidity in today's market environment.

Is illiquidity premium slowly eroding?

Let's examine both sides of the argument and what investors should really be thinking about when allocating to private markets. More importantly, we'll discuss the only meaningful predictor of outsized returns.

📚 You’ll find additional resources and further reading at the end of the article.